Inventory Expands Across the Austin Housing Market

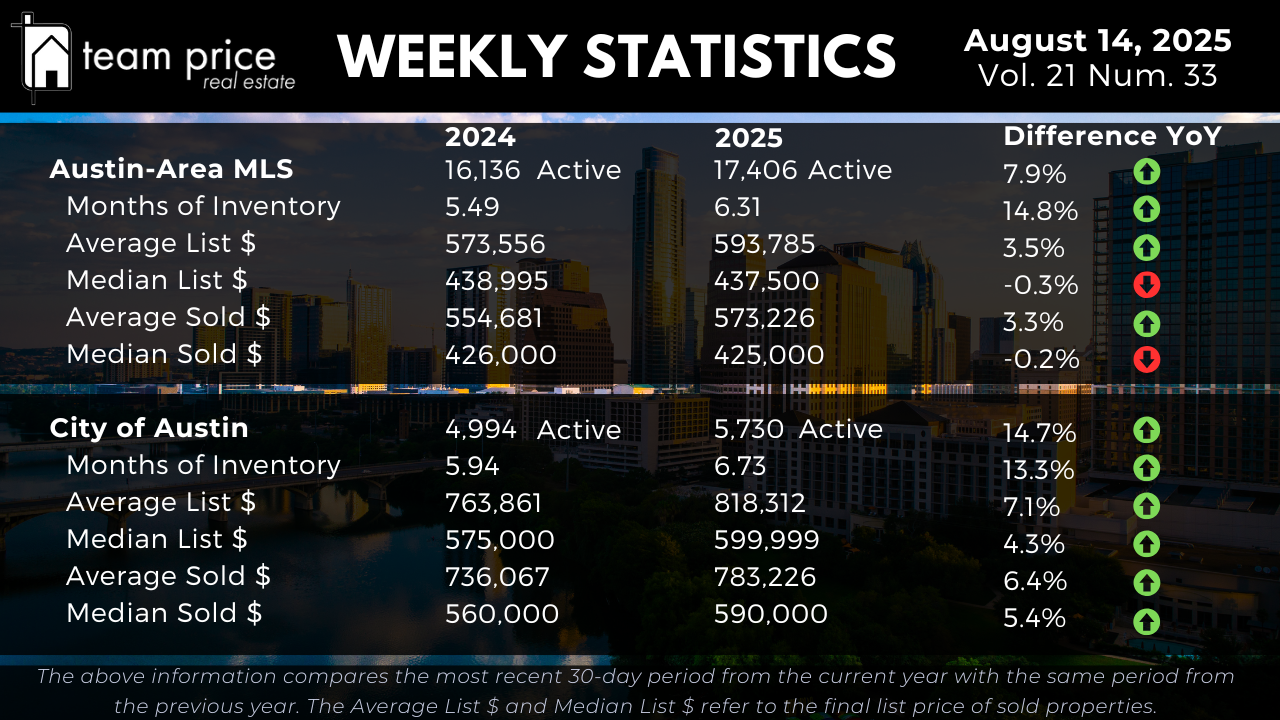

The Austin real estate market continues to shift toward a more balanced environment. Across the Austin-Area MLS, active residential listings have climbed to 17,406, up 7.9% from 16,136 at the same time last year. Months of Inventory now stands at 6.31, compared to 5.49 a year ago — a 14.8% increase that reflects a 1.1× expansion in supply relative to the current pace of sales. Within the City of Austin, the supply increase has been even more significant. Active listings rose from 4,994 to 5,730, a 14.7% gain, while Months of Inventory increased from 5.94 to 6.73, up 13.3% year over year. This steady growth in available homes gives buyers more options and eases some of the urgency that characterized the market in recent years.

Austin Housing Prices Show Diverging Trends

Price trends across the Austin-Area MLS highlight a split between average and median values. The average list price rose 3.5% to $593,785, and the average sold price increased 3.3% to $573,226. In contrast, the median list price fell 0.3% to $437,500, and the median sold price dipped 0.2% to $425,000. This pattern suggests that higher-priced sales are helping lift averages, while mid-tier home values remain flat. In the City of Austin, pricing strength is more consistent. The average list price is up 7.1% year over year to $818,312, and the median list price has climbed 4.3% to $599,999. On the sales side, the average sold price rose 6.4% to $783,226, while the median sold price increased 5.4% to $590,000. These gains point to greater resilience inside city limits compared to the broader region.

Regional and ZIP Code-Level Market Performance

Market conditions vary widely across Central Texas. Among the 30 tracked cities, 40% saw month-over-month median price gains in August, while 57% recorded declines. On a year-over-year basis, only 33% of cities posted price increases, with 67% reporting decreases. None have surpassed their 12-month price peak. At the ZIP code level, the distribution is similar. Of the 75 areas analyzed, 45% reported month-over-month gains, 51% declined, and 4% held steady. Year over year, 48% are up and 52% are down. Only one ZIP code has exceeded its 12-month high, underscoring how widespread the price normalization has been since earlier market peaks.

Negotiation and Seller Concessions Becoming Standard

Most homes are now selling below their original asking price. In August, 69.43% of closed sales were below list price, compared to 65.95% last month. The share of homes selling at list price dropped from 21.86% to 18.21%, while 12.36% sold above list — a figure that has held steady month to month but is down from July 2024’s 13.21%. The average sold-to-list price ratio sits at 97.05%, reflecting a market where negotiation is common and seller flexibility is often required to secure a sale.

Prices Remain Below Peak Levels

Despite some recent gains, prices remain well below their highs from 2022 and early 2025. In the Austin-Area MLS, the average list price is down 11.5% from its April 2025 peak, and the median list price is 16.7% below its May 2022 high. The average sold price is 9.6% lower than its peak, while the median sold price is down 19.2%. Price-per-square-foot metrics have dropped 21.9% (average) and 23.2% (median) from their 2022 highs.

In the City of Austin, the average list price is 17.2% below its April 2024 peak, and the median list price is 17.2% under its May 2022 high. The average sold price is only 2.3% below its May 2022 peak, but the median sold price is still down 14.1%. Price per square foot has fallen by more than 22% compared to its previous high.

What This Means for Buyers, Sellers, Investors, and Agents

For buyers, the increase in inventory and longer market times translate to more choices, better negotiation opportunities, and less pressure to make quick decisions. Median prices in many areas are flat or slightly down, which could open doors to better value, especially outside the city core.

For sellers, competition has increased, and pricing strategy matters more than ever. Homes priced appropriately for the market are still selling, but the high percentage of below-list-price transactions shows that many sellers need to adjust expectations.

For investors, the current market offers the chance to acquire properties at prices still well below recent peaks. While rent growth has cooled, the combination of lower purchase prices and steady demand in key neighborhoods may present attractive long-term opportunities.

For real estate agents, understanding hyperlocal trends is critical. With conditions varying widely between ZIP codes and even within neighborhoods, guiding clients with precise, data-backed advice will be the key to success in the months ahead.