Austin Housing Market FAQ – October 02 2025

1. What is the latest update on the Austin housing market?

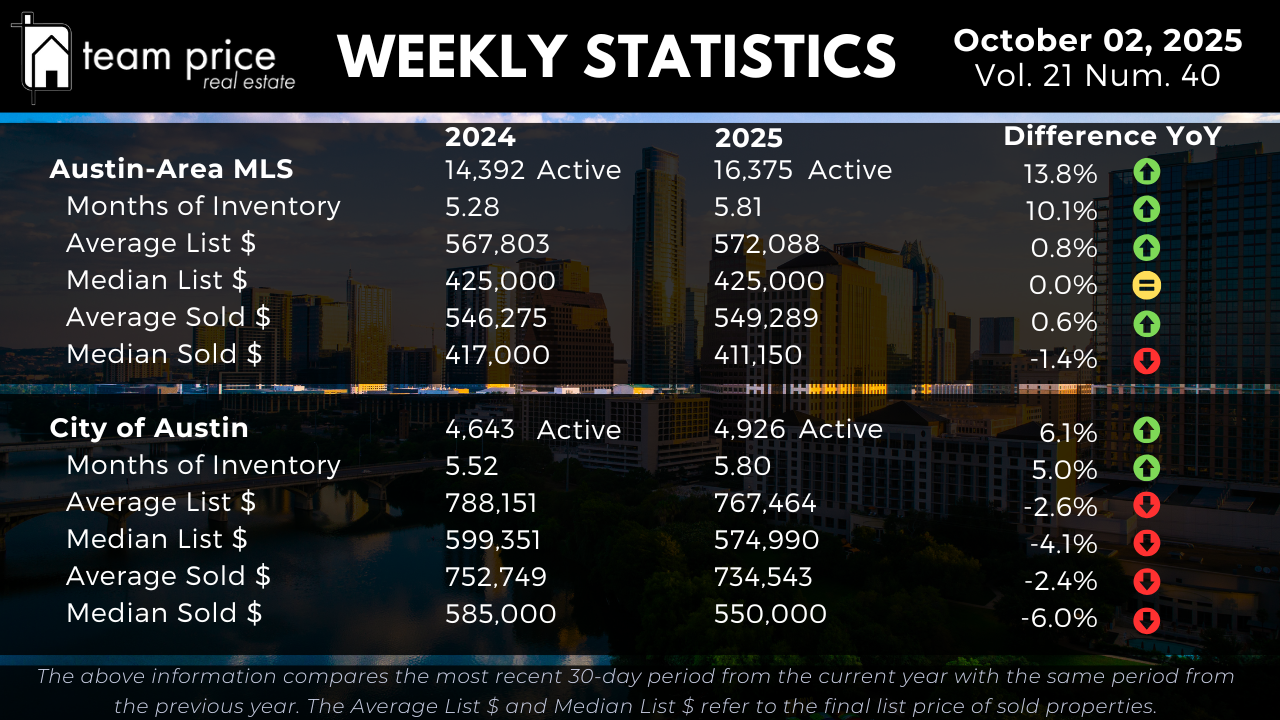

As of October 02 2025, the Austin-Area MLS is showing elevated inventory alongside flat-to-soft pricing trends. Active listings have risen to 16,375, up 13.8 percent from 14,392 one year ago, and Months of Inventory has expanded from 5.28 to 5.81, a 10.1 percent increase. The average list price is $572,088, which is up 0.8 percent year over year, while the median list price is unchanged at $425,000. On the sales side, the average sold price is $549,289, a modest 0.6 percent gain, but the median sold price has slipped 1.4 percent to $411,150. Within the City of Austin, the numbers show even more pressure. Inventory has grown by 6.1 percent and Months of Inventory has increased to 5.80, while prices are clearly down. The average list price is off by 2.6 percent, the average sold price has fallen by 2.4 percent, and the median sold price has dropped sharply by 6 percent compared to last year.

2. Why are Austin home prices dropping?

Austin home prices are softening because the market is experiencing a significant rise in supply combined with slower absorption. Inventory in the Austin-Area MLS has grown by nearly 14 percent, and in the city by over 6 percent, meaning more homes are competing for a limited pool of buyers. Months of Inventory has also risen, showing that homes are taking longer to sell. This higher supply is giving buyers more choices and reducing the urgency that once pushed prices higher. Inside the city, affordability constraints and competition from suburban and new-build markets are intensifying the pressure. Sellers are also conceding more during negotiations, with the average sold-to-list price ratio now at 96.67 percent, a clear indicator that buyers are securing discounts. These dynamics together explain why values, particularly median prices in Austin proper, are heading lower.

3. What is the trend in Austin real estate in 2025?

The 2025 trend for Austin real estate is one of transition toward balance after several years of extreme seller-favored conditions. Rising inventory is outpacing buyer demand, pushing Months of Inventory higher and easing price momentum. Across the Austin-Area MLS, pricing is essentially flat, with average values holding steady and median prices down slightly. Inside the City of Austin, declines are sharper, especially at the median level, signaling affordability issues and less aggressive buyer activity. The overall market is not in freefall but is clearly adjusting, with buyers gaining negotiating leverage and sellers being forced to reset expectations. In short, the market is moving away from rapid appreciation toward a more measured, balanced environment.

4. Should I buy a house now or wait for a recession?

Whether to buy now or wait depends heavily on personal circumstances, but the data suggests there are reasons to consider purchasing today. Inventory is at its highest level in years, giving buyers more choice and leverage in negotiations, with most sales closing under list price. The Austin-Area MLS median sold price has already slipped 1.4 percent year over year, and in the City of Austin, the median has dropped 6 percent, meaning many buyers are securing better deals than they could a year ago. Waiting for a recession is uncertain, since economic conditions, interest rates, and supply trends can shift quickly, and higher mortgage rates could offset any future price declines. For buyers who are financially prepared and plan to hold long-term, today’s balanced market offers opportunities that did not exist during the height of the boom.

5. Is Austin’s housing boom over?

The explosive boom that defined the Austin housing market in recent years has cooled, and the data confirms that the period of double-digit appreciation is behind us. Inventory is significantly higher than a year ago, absorption has slowed, and median prices in the city have fallen by six percent. Across the broader MLS, pricing is mostly flat, while city values are clearly trending lower. This shift does not mean the market is collapsing, but it does show that Austin has moved into a new phase defined by balance rather than frenzy. The boom may be over, but what remains is a healthier, more sustainable market that favors buyers, challenges sellers, and provides investors with opportunities to acquire at levels that are 15 to 25 percent below peak.